Diane Prescott spent thirty-one years teaching seventh-grade English in a public school district outside of Toledo, Ohio. She retired at sixty-four with a pension that covered roughly half her monthly expenses, a Social Security benefit she had not yet claimed, and $152,000 in a 403(b) retirement account. By the standards of most retirement calculators, her situation looked bleak. The projections told her she would run out of money by age eighty-two. Diane is now seventy-three, and her plan is working better than any of those projections suggested it would.

The turning point was not a windfall or a lucky investment. It was a decision -- specifically, the decision to delay claiming Social Security from age sixty-four to age sixty-seven. That three-year delay increased her monthly benefit by approximately twenty-four percent, adding roughly $480 per month to her guaranteed lifetime income. Over a twenty-year retirement, that single timing decision is worth more than $115,000 in additional benefits.

To bridge the gap between retirement and her delayed Social Security claim, Diane allocated $45,000 of her savings into a fixed annuity that paid a guaranteed monthly amount for exactly thirty-six months. It was not glamorous. The interest rate was modest. But it served its purpose with mechanical precision: it covered her expenses during the years she was not yet drawing Social Security, without requiring her to touch the rest of her savings.

The remaining $107,000 stayed invested in a balanced fund -- sixty percent stocks, forty percent bonds. Because Diane was not withdrawing from this account during its most vulnerable early years, the portfolio had time to grow. By the time she turned sixty-seven and her full Social Security benefit began, her invested balance had grown to approximately $128,000 despite contributing nothing additional.

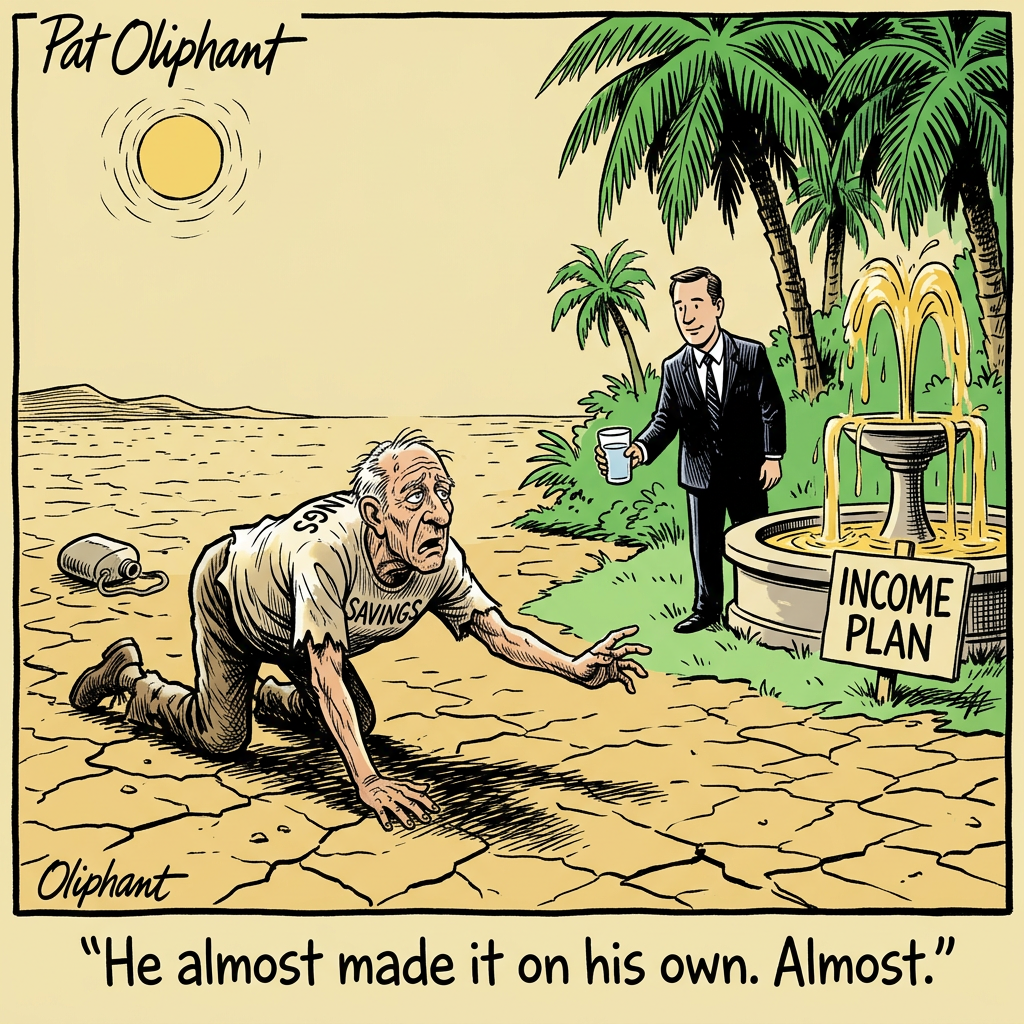

Here is what Diane understood that many retirees with far more money do not: the size of your savings matters less than how strategically you deploy them. A $150,000 portfolio with a clear plan will often outperform a $500,000 portfolio managed by hope and improvisation.

The trade-off deserves acknowledgment. Diane lives modestly. She does not take European vacations or drive a new car. Her plan eliminated the risk of running out of money, but it did not create abundance. This is an honest distinction that matters. A well-designed retirement plan for modest savings means security, not luxury. Anyone who promises otherwise is selling something.

What Diane's story illustrates is that retirement planning is not exclusively a wealthy person's concern. The tools available -- Social Security timing, small annuity allocations, disciplined investment -- work at every income level. The mathematics are the same whether your portfolio has six figures or seven. The question is whether you use them deliberately or leave them to chance.

Diane Prescott did not pray for a miracle. She made a plan. Nine years later, that plan is still paying her bills, still covering her medications, and still letting her sleep through market corrections without a second thought. For a retired English teacher from Toledo, that is more than enough.