There is a particular kind of financial loss that never appears on any statement. It is not a market crash. It is not a bad investment. It is not even a scam. It is the slow, invisible erosion of options that occurs when someone who knows they should act simply does not. Behavioral economists call it the status quo bias -- the deeply human preference for inaction over action, even when inaction carries a measurable cost. In retirement planning, this bias is quietly responsible for more financial damage than any single market event in modern history.

Consider what happens when a sixty-year-old decides to "think about" retirement planning and revisits the idea at sixty-five. In those five years, the cost of purchasing guaranteed lifetime income has increased by roughly fifteen to twenty-five percent, because annuity pricing is based on age and prevailing interest rates. The same monthly income that could have been secured at sixty for $200,000 may now require $240,000 or more. The money did not disappear. The opportunity did.

Social Security optimization follows the same pattern. The window for making strategic claiming decisions is finite and non-renewable. A married couple at age sixty-two has dozens of possible claiming combinations, many of which differ by $100,000 or more in total lifetime benefits. By age sixty-six, many of those options have expired. By seventy, the decision has been made by default -- often in the least advantageous way possible.

Health insurance bridges, long-term care planning, Roth conversions during low-income years, pension buyout decisions -- each of these has a window. Each window closes on a schedule that is indifferent to whether you were paying attention. The retirement planning landscape is not a buffet that stays open indefinitely. It is a series of time-limited offers that expire whether or not you have read the menu.

What makes procrastination uniquely dangerous in this context is that it does not feel like a decision. Selling a stock at a loss feels like a decision. Choosing a high-fee fund feels like a decision. But deciding to "wait until next year" feels like nothing at all. That is precisely why it is so destructive. The person who waits does not experience the cost of waiting in real time. They experience it years later, when an advisor explains what was once possible and is no longer available.

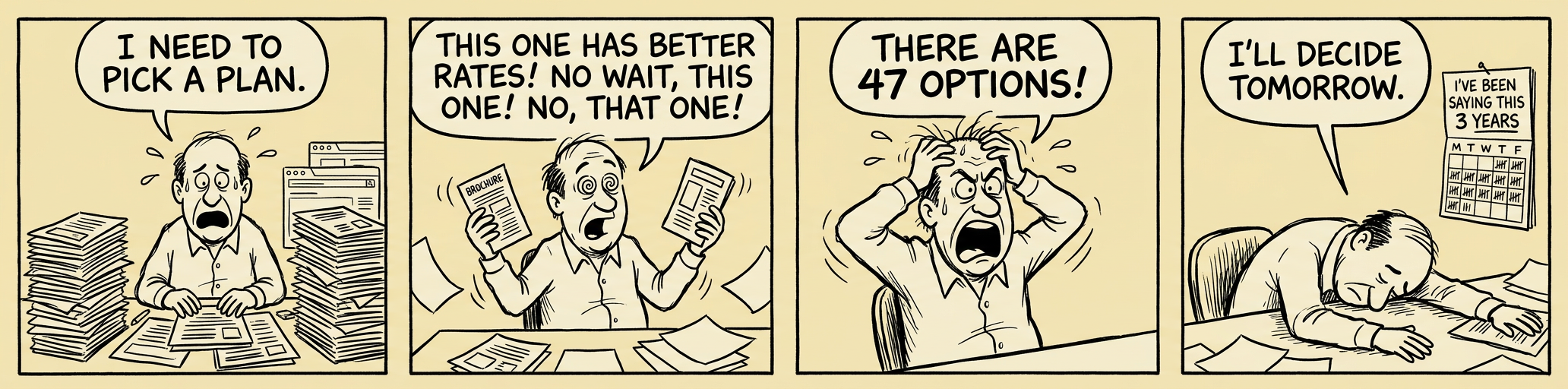

The financial services industry bears some responsibility here. Retirement planning is often presented as an overwhelming, all-or-nothing proposition. People who cannot do everything do nothing. But the research is clear: partial action dramatically outperforms inaction. A single conversation with a qualified advisor -- even without implementing a single recommendation -- changes retirement outcomes measurably, because it moves the individual from unconscious default to conscious awareness.

Here is the trade-off worth acknowledging: taking action requires confronting uncertainty, and that is genuinely uncomfortable. It means looking at numbers that may be sobering. It means admitting that you do not know everything. It means trusting a process that cannot guarantee a perfect outcome. These are real psychological costs. But they are temporary costs that purchase permanent benefits. Procrastination offers the opposite bargain: temporary comfort that purchases permanent limitation.

The retirees who fare best are not the ones who made perfect decisions. They are the ones who made timely decisions -- imperfect, revisable, good-enough decisions made while the window was still open. The biggest mistake is not choosing the wrong plan. It is arriving at retirement with no plan at all and discovering that the best options expired while you were thinking it over.