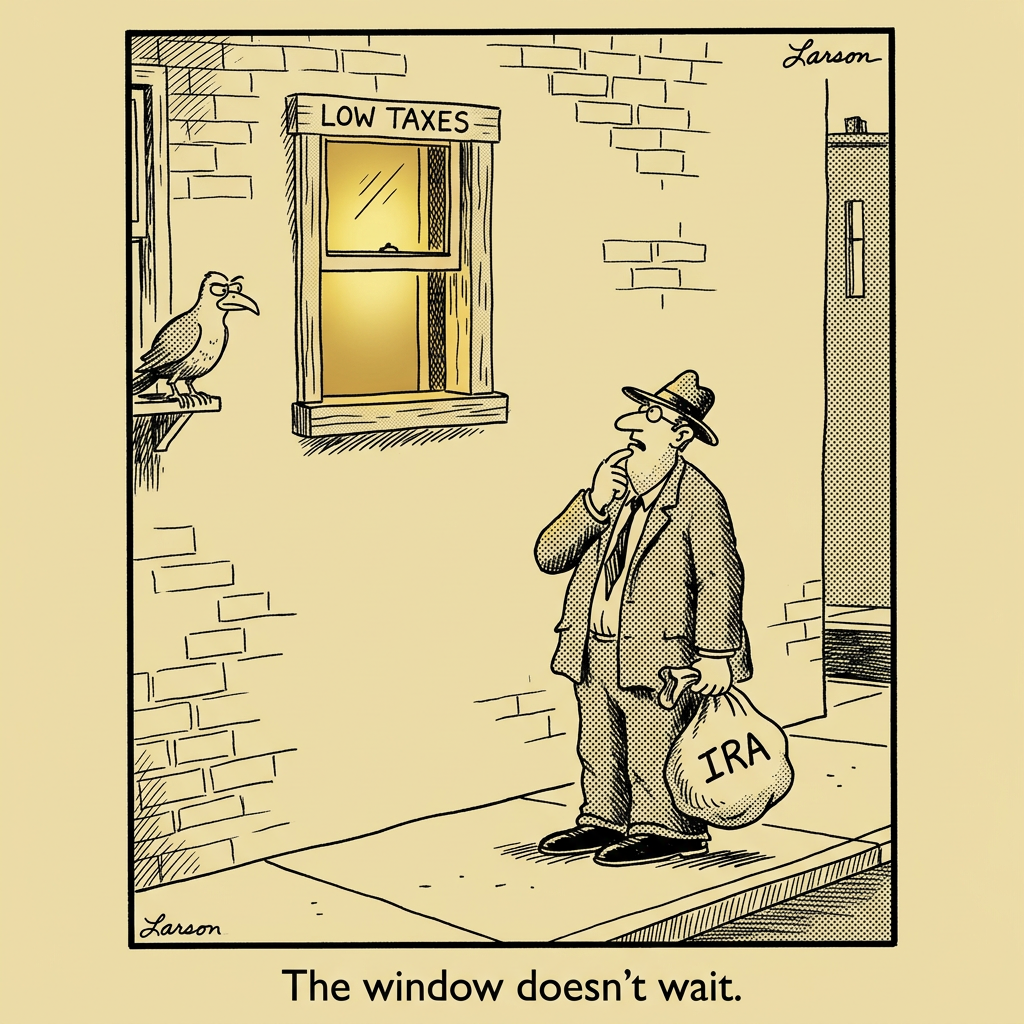

There is a quiet period in most retirees' financial lives that tax professionals call "the golden window." It begins the day you stop earning a paycheck and ends the day you turn 73, when the IRS requires you to start pulling money from your traditional retirement accounts. During those years, your taxable income often drops to the lowest level you will see for the rest of your life. And most people do absolutely nothing with it.

That inaction is not laziness. It is the natural result of a financial system that never taught you to think about taxes in retirement. You spent forty years focused on accumulating money. Nobody explained that the decade after your last day of work might be the single most important tax-planning period of your entire financial life.

Consider what happens if you retire at 63 with $800,000 in a traditional IRA. You are living on Social Security and perhaps a small pension. Your taxable income is modest. But at 73, the government will force you to withdraw roughly $31,000 per year from that IRA — whether you need the money or not. That withdrawal gets stacked on top of your Social Security benefits, potentially pushing you into a higher tax bracket and triggering taxes on income that was previously untaxed.

The move most people miss is the Roth conversion. During those low-income years between retirement and 73, you can strategically convert portions of your traditional IRA into a Roth IRA. Yes, you pay income tax on the amount you convert. But here is the part that changes the math entirely: you pay that tax at today's lower rate, and every dollar in the Roth grows tax-free for the rest of your life. No required minimum distributions. No tax on withdrawals. No impact on your Social Security taxation.

The trade-off is real and worth acknowledging. You will write a check to the IRS in a year when you did not have to. That feels wrong to most people. It feels like volunteering for a tax bill. But the alternative is waiting until 73 and paying taxes at a potentially higher rate, on a potentially larger balance, with no ability to control the timing or amount.

There is a second move that compounds the benefit. The order in which you draw from your accounts matters enormously. Most retirees default to spending taxable accounts first, then tax-deferred, then Roth. Research from financial planning firms suggests that a carefully sequenced withdrawal strategy — one that coordinates which accounts you tap in which years — can extend the life of your portfolio by several years and reduce your lifetime tax burden by tens of thousands of dollars.

The challenge is that none of this is intuitive. The tax code does not come with a retirement chapter that explains the optimal sequence. Your accountant files last year's return. Your old 401(k) administrator sends a statement. Nobody is connecting the dots between your current tax bracket, your future RMD obligations, and the opportunity sitting in front of you right now.

That is what a proper retirement education session is designed to address. Not selling you a product, but showing you the map — where the windows are, when they close, and what it costs to miss them.